My Broker Mailed a 1099 That Triggered a $9,000 IRS Penalty

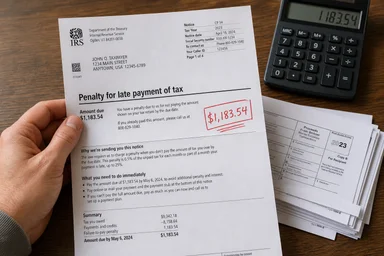

Last April, a retired engineer in Ohio opened a letter from the IRS that made him spill his morning coffee. The notice demanded $9,000 in penalties for underpaying estimated taxes. He had never missed a payment before. The culprit was a single 1099 from his brokerage, which reported a $50,000 short-term capital gain from a stock sale in December. He had sold the shares to raise cash for a home renovation, but the gain was far larger than he expected because of a wash sale earlier that year. The broker had disallowed a $15,000 loss from a repurchase within 30 days, turning what should have been a $35,000 gain into $50,000 on paper. The IRS penalty was the final sting.

The Surprise Letter That Cost $9,000

The engineer, let's call him Mark, had always paid his taxes through withholding from his pension and Social Security. He rarely traded, so he never bothered with quarterly estimated payments. But in 2023, he sold a chunk of a tech stock that had soared. He figured the tax would come out of his refund or he'd pay it by April 15. He didn't realize that the IRS expects taxpayers to pay most of their income tax during the year, not in one lump sum.

The penalty was calculated using IRS Form 2210. Because Mark's income spiked, he didn't meet any of the safe harbor rules. The safe harbor generally requires you to pay either 90% of the current year's tax or 100% of the prior year's tax (110% if your adjusted gross income was over $150,000). Mark's prior year tax was $12,000, so he should have paid at least $13,200 in estimated payments. He paid zero. The penalty for underpayment is roughly the federal short-term rate plus 3 percentage points, which as of late 2024 was around 8% per year, compounded daily on each missed installment.

Many investors assume that if they have a big gain in December, they can just pay the tax by January 15 of the next year. That's true for the final quarterly estimated payment, but if you had income earlier in the year, you needed to pay by April 15, June 15, and September 15 as well. The penalty is calculated on each quarter's shortfall separately. Mark's gain was in December, so only the January 15 payment was affected, but the penalty still added up because the tax owed was large.

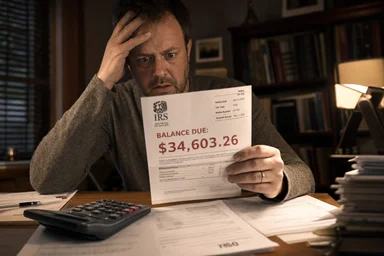

The notice gave Mark 30 days to respond. He could either pay the $9,000 or request a penalty abatement. He had never used the first-time abate rule, which the IRS grants to taxpayers with three years of clean compliance. Mark qualified. He wrote a letter explaining his misunderstanding, and the IRS waived the penalty. But not everyone gets that lucky. If you have had a penalty in the past three years, you are ineligible.

How Wash Sales Inflate Your Tax Bill

Mark's $50,000 gain was partly an illusion. He had bought the stock in January for $100,000, sold it in March for $85,000 (a $15,000 loss), and then bought it again in April for $82,000. That repurchase within 30 days triggered the wash sale rule. The $15,000 loss was disallowed and added to the cost basis of the new shares. When he sold those shares in December for $132,000, his basis was $82,000 plus the disallowed loss of $15,000, or $97,000. But the broker's 1099 reported the sale proceeds of $132,000 minus the original cost basis of $82,000, showing a $50,000 gain. The disallowed loss was buried in a footnote.

The wash sale rule is designed to prevent investors from selling a losing position for a tax benefit and immediately buying it back. But it can create phantom gains if you don't track the adjusted basis. The IRS treats the disallowed loss as added to the new shares' cost, so eventually you get the deduction when you sell those shares and don't repurchase within 30 days. But if you sell in a different tax year, the loss is deferred. In Mark's case, the loss was realized in the same year, but the broker's reporting made it look like a larger gain.

Short-term capital gains are taxed at ordinary income rates, which for Mark in the 24% bracket meant a $12,000 federal tax bill on the $50,000 gain. If the gain had been long-term (held over one year), the rate would have been 15%, saving $4,500. But Mark had held the shares only eight months. The wash sale also reset the holding period, so the second lot was short-term. This is a common trap: investors who trade frequently may find their gains treated as short-term even if they held the original shares for years.

To avoid wash sales, you can wait 31 days before repurchasing a substantially identical security. Or you can buy a different security that is not substantially identical, such as an ETF that tracks a different index. Some investors use tax-loss harvesting to offset gains, but they must be careful not to trigger a wash sale. Many robo-advisors automate this, but they can still make mistakes if you manually trade the same security.

The Timing Trap of Mutual Fund Distributions

Mutual funds and ETFs often distribute capital gains and dividends in December. If you buy a fund just before the ex-dividend date, you pay tax on the distribution even though you didn't earn the underlying gains. This is known as "buying the dividend." For example, Vanguard Total Stock Market Index Fund (VTSAX) paid a capital gain distribution of roughly $1.50 per share in December 2022. A $10,000 investment would have triggered about $150 in taxable income, even if the fund's price dropped by a similar amount after the distribution.

These distributions can be large in years when fund managers rebalance or sell appreciated holdings. In 2021, some actively managed funds distributed over 10% of their net asset value as capital gains. Index funds tend to have smaller distributions, but they are not immune. The Vanguard 500 Index Fund (VFIAX) distributed about $2.30 per share in December 2023, creating a tax liability for new investors who bought in November.

If you are investing in a taxable account, check the fund's distribution schedule. Most fund companies post estimated distribution dates in November. You can avoid the tax by waiting until after the ex-dividend date to buy. Or you can hold the fund in a tax-advantaged account like an IRA, where distributions are not taxed annually. But if you need the money in a taxable account, timing matters.

The IRS does not penalize you for receiving distributions; you simply pay tax on them. But if the distribution pushes your income higher than expected, you may owe estimated tax penalties. For example, if you normally owe $5,000 in tax and a $1,000 distribution triggers an extra $250, you might not meet the safe harbor. This is especially tricky for retirees who have fixed withholding from pensions and may not adjust for mutual fund income.

Estimated Tax Rules and Safe Harbor: A Closer Look

The IRS requires taxpayers to pay income tax as they earn income. For wage earners, that's done through withholding. For investors, it's done through quarterly estimated payments. The due dates are April 15, June 15, September 15, and January 15 of the following year. Each payment covers income received during that quarter. If you have a big gain in December, you can make a payment by January 15 to cover it. But if you had gains in March, you needed to pay by April 15.

The penalty is calculated using Form 2210, which compares your actual payments to what you should have paid based on your income each quarter. There are exceptions. The safe harbor rule lets you avoid a penalty if you pay at least 110% of your prior year's tax (if your AGI was over $150,000) or 100% (if under). If your income drops, you can use the annualized income installment method, which aligns payments with when you earned the income. But that method requires filing Form 2210 Schedule AI, which is complex.

As of late 2024, the IRS interest rate for underpayments is 8% per year, compounded daily. That's higher than many credit cards. For a $10,000 underpayment that lasts nine months, the penalty is about $600. But the penalty is separate from interest; you may owe both. The IRS calculates the penalty for each quarter separately, so a late payment in Q1 accrues penalty until the tax is paid.

Many investors ignore estimated taxes because they think the penalty is small or they will make it up with a refund. But the penalty can be substantial if the underpayment is large. Some CPAs recommend setting up automatic quarterly payments to avoid the hassle. Others suggest increasing withholding from a paycheck or pension, because withholding is treated as paid evenly throughout the year, even if you withhold extra in December. This is a simple workaround: adjust your W-4 to withhold an extra $500 per paycheck, and you can cover a large gain without estimated payments.

However, there are situations where paying estimated taxes may not be necessary. For example, if you have a low-income year, you might fall below the filing threshold or owe little tax. In that case, the safe harbor rule may still protect you if your prior year's tax was low. Conversely, if your income is highly variable, the annualized income installment method can reduce penalties by matching payments to income timing. But this method requires careful record-keeping and may be impractical for some. For instance, a freelance consultant who receives a large payment in December can use Schedule AI to show that no income was earned in earlier quarters, thereby avoiding penalties for those quarters. This trade-off between simplicity and precision is worth considering.

Three Red Flags on Your Broker's 1099

The 1099 form your broker sends each year contains several boxes that can trigger surprises. Box 1a reports total ordinary dividends. If that number is higher than expected, you may have received dividends from funds you forgot you owned. Box 2a reports total capital gain distributions from mutual funds. These are passed-through gains from the fund's trading, and they are taxable to you even if you reinvested them. Box 3a reports qualified dividends, which are taxed at lower capital gains rates. But if you held the stock for less than 61 days, the dividend is not qualified and is taxed as ordinary income.

Box 6 reports foreign tax paid, which may entitle you to a foreign tax credit. But you have to itemize deductions to claim it, or use Form 1116. Many investors miss this and overpay. Box 12 (or Box 14 on some forms) reports crypto transactions if your broker handles digital assets. The IRS treats crypto as property, so every sale or exchange is a taxable event. If you received a 1099 for crypto, you may owe tax on gains you didn't realize were taxable.

Another red flag is the wash sale indicator. Some brokers mark transactions that are wash sales, but they may not adjust the cost basis correctly. You should review the 1099 for any footnote about disallowed losses. If you see a large gain that seems out of line with your trading, check if a wash sale inflated it. You can also request a corrected 1099 if the broker made an error, but you have to catch it before April 15.

Finally, look at the summary of proceeds (Form 1099-B). It shows the cost basis reported to the IRS. If you transferred shares from another broker, the basis may be wrong. The IRS expects you to report the correct basis, not necessarily what the broker shows. If you have a loss, you can claim it even if the broker shows a higher gain, but you need documentation.

How to Hedge Against a Penalty Next Year

The simplest way to avoid an estimated tax penalty is to adjust your withholding. File a new W-4 with your employer or pension payer, requesting an extra dollar amount withheld each pay period. You can also have your broker withhold taxes from sales, but that is rare. Withholding is treated as paid evenly throughout the year, so you can fix a mid-year gain by increasing withholding in the last months. For example, if you have a $20,000 gain in September, you can increase your withholding from October to December to cover the additional tax, avoiding a penalty for Q3.

If you have a large gain late in the year, you can increase your final estimated payment due January 15. This covers the gain from the fourth quarter. But be aware: if you had gains earlier in the year, you may still owe a penalty for earlier quarters. To avoid that, you can use the annualized income method when filing your tax return. This method lets you pay based on when you earned the income, so a late-year gain doesn't trigger a penalty for Q1–Q3. For instance, using Schedule AI in tax software like TurboTax or H&R Block, you can input the exact dates of your income and calculate the correct installment amounts.

Tax-loss harvesting before year-end can offset gains. If you have unrealized losses in your portfolio, you can sell them to realize the loss and offset any realized gains. The loss must be in a taxable account, and you cannot repurchase the same security within 30 days (wash sale rule). Many investors harvest losses in November and December. Some brokerage platforms offer automated tax-loss harvesting, but you should review the trades to ensure they don't create wash sales with other holdings. For example, Betterment's tax-loss harvesting service automatically sells losing positions and buys similar but not identical ETFs to maintain market exposure.

Finally, set calendar reminders for estimated tax due dates. The IRS does not send reminders. If you miss a payment, you can still make it up by the next due date, but the penalty for the missed quarter will accrue. Some investors prefer to pay 110% of the prior year's tax in four equal installments, which guarantees no penalty regardless of current year income. This works well if your income is stable or declining. If your income rises, you may owe additional tax, but no penalty.

When a CPA Can Save You More Than They Cost

If you receive an IRS penalty notice, a CPA can often get it reduced or waived. The first-time penalty abatement rule applies to taxpayers who have not had any penalties in the prior three years and have filed all required returns. You can request abatement by phone or by letter. The IRS grants abatement in roughly 60% of cases, according to some estimates. A CPA can draft a reasonable cause letter if you had a medical emergency, natural disaster, or other circumstance.

Even if you don't qualify for first-time abatement, you can request a partial waiver. The IRS may reduce the penalty if you show that you made a good-faith effort to comply. For example, if you made estimated payments but miscalculated, you can argue that the underpayment was not willful. The IRS has some discretion. A CPA familiar with the process can increase your chances.

The cost of hiring a CPA to handle a penalty notice is typically $300 to $500 for a simple letter. If you need to file an amended return or Form 2210, it may cost more. But compared to a $9,000 penalty, it's a bargain. Many CPAs offer a free initial consultation to review the notice and tell you if abatement is likely. You can also use tax software to generate the abatement request, but the IRS may be more responsive to a professional letter.

In Mark's case, a CPA could have spotted the wash sale issue before he sold the stock. The CPA might have advised him to wait 31 days to avoid the wash sale, or to sell a different lot. Looking back, proactive tax advice could have saved him from the penalty entirely. If you trade actively or have a large portfolio, a CPA may pay for itself in avoided penalties and tax savings.

Consider whether a CPA is right for you. For simple situations, tax software may suffice. But for complex portfolios or unexpected 1099 surprises, professional guidance can prevent costly mistakes. Review your tax situation annually and consult a professional if you have questions.

Disclaimer: This article is for informational purposes only and does not constitute tax advice. Consult a qualified tax professional for your specific situation.