How my health savings account tax error cost me $638

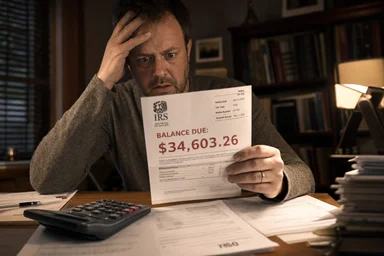

It arrived in an official envelope with a Kansas City return address. I knew it wasn't a refund. The IRS notice, dated December 2023, informed me that I owed $638.42 for an excess health savings account contribution. The mistake? I missed a corrective deadline by 48 hours. That two-day gap turned a fixable overcontribution into a permanent penalty. This is the story of how one overlooked form and a misunderstood rule cost me real money — and how you can avoid the same fate.

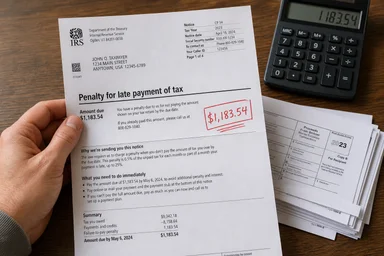

The $638 surprise that started it all

The notice was CP2000, the IRS's way of saying “we think you underpaid.” It listed a $1,200 excess HSA contribution for 2023, plus a 6% excise tax for the first year, plus back taxes on the ineligible amount. Total due: $638.42. I had opened the HSA in January 2023, contributed the full individual limit of $3,850, and assumed everything was fine. I was wrong.

The problem began when I left my job in November 2023. My employer had offered a high-deductible health plan (HDHP) paired with an HSA. I enrolled in January and contributed monthly. When I resigned, I lost HDHP coverage at the end of November. I didn't think much of it — I had been covered for 11 months, so I assumed I could keep the full year's contribution. That assumption was my first error.

The IRS requires that you be eligible to contribute to an HSA for each month you want the contribution to count. But there's a special rule, called the last-month rule, that lets you contribute the full annual limit if you are covered by an HDHP on December 1. However, there's a catch: you must remain covered for the entire following year — all 12 months of 2024 — or the contribution becomes excess. I didn't know that.

I missed the corrective deadline by 48 hours. The IRS allows you to withdraw the excess contribution plus earnings before the tax-filing deadline (including extensions) to avoid the penalty. My tax return was filed on April 15, 2024, but I didn't realize the error until December. By then, the window had closed. The $1,200 excess was now subject to a 6% excise tax every year until corrected. That first year's penalty was $72, plus the back taxes on the amount that should never have been in the account.

How HSA tax rules trip up even careful savers

Health savings accounts offer a triple tax advantage: contributions are deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. But that generous tax treatment comes with strict eligibility rules. To contribute, you must be covered by a high-deductible health plan (HDHP) and not be enrolled in Medicare or claimed as a dependent. The contribution limit for 2023 was $3,850 for individual coverage and $7,750 for family coverage.

Where many people stumble is the requirement that you must be eligible for the entire month to count that month. If you lose HDHP coverage mid-month, you are not eligible for that month. The IRS uses a “months of eligibility” calculation to cap contributions. For example, if you are covered for 11 months, your limit is 11/12 of the annual maximum. That proration is easy to overlook when you change jobs midyear.

Spouse coverage adds another layer. If your spouse has a family HDHP, you may both be covered under that plan, but the contribution limit is shared. A common error is each spouse contributing the full family limit, resulting in an excess. The IRS Form 8889, which you file with your tax return, is where these calculations happen. Line 3 asks for the number of months you were eligible. Fill it wrong, and the rest of the form cascades into error.

Even careful savers miss details. A 2022 study by the Employee Benefit Research Institute found that roughly 15% of HSA accountholders had excess contributions in a given year, often due to job changes or midyear coverage switches. The IRS audits a small fraction, but the notices that do go out are expensive. My $638 penalty is modest compared to some stories I've heard — people have racked up thousands in excise taxes and back taxes from years of unnoticed excess contributions.

My mistake: ignoring the last-month rule

The last-month rule is a provision in IRS Publication 969 that allows you to treat yourself as eligible for the entire year if you are covered by an HDHP on December 1. It's designed to let people who start HDHP coverage late in the year still contribute the full annual limit. But it comes with a 12-month testing period: you must remain covered by an HDHP for all of the following year. If you don't, the contribution becomes excess retroactively.

When I left my job in November 2023, I was covered on December 1. So the last-month rule applied. That meant my full $3,850 contribution was initially valid. But because I did not have HDHP coverage for any month in 2024 — my new job offered a PPO, not an HDHP — I failed the testing period. The $1,200 I contributed after September (the month I would have been ineligible under proration) became excess.

I had assumed that the last-month rule was a one-time check: if you're covered on December 1, you're good. I didn't realize the testing period extended into the next year. The IRS publication is clear, but it's buried in dense paragraphs. I had read it — or thought I had — but I missed the testing period requirement. That was my second error: not verifying the rule with a qualified professional or at least a second source.

Had I known, I could have either withdrawn the excess before the tax deadline or maintained HDHP coverage through 2024. Neither happened. The corrective deadline passed, and the penalty stuck. The IRS notice arrived in December, a full eight months after the deadline, but the clock had already run out.

The math behind the penalty

The penalty calculation is straightforward but painful. For 2023, I overcontributed $1,200. The IRS imposes a 6% excise tax on excess contributions that remain in the account after the corrective deadline. That's $72 for the first year. But the excise tax applies every year the excess stays in the account, so if I don't remove it, I'll owe another $72 for 2024, 2025, and so on.

On top of the excise tax, the IRS also taxes the earnings on the excess contribution. In my case, the $1,200 grew to about $1,260 by the time I received the notice. The $60 gain is taxable income for 2023, and since it was in an HSA, it's not reported until you withdraw it. But the IRS treats the entire $1,200 as if it were never in an HSA, so the earnings are also out of the tax shelter. I owed about $15 in additional income tax on those earnings, plus a small penalty for late payment.

The total bill was $638.42, broken down as: $72 excise tax, $15 additional income tax, $8 late-payment penalty, and $543.42 in interest — the bulk of which came from the IRS's calculation of underpayment interest from the original due date. Interest rates were around 7% in 2024, so the interest accumulated quickly over the 20 months between the original filing deadline and the notice date.

Some people argue that the 6% excise tax is manageable — it's only $72 on a $1,200 excess. But the compounding effect over multiple years can be significant. If I had left the excess in for 10 years, the excise tax alone would be $720, plus interest on the back taxes. And if the account grows, the earnings are also taxed. The real cost is the lost opportunity: that $1,200 could have been invested in a taxable account or used for medical expenses. Instead, it's stuck in a penalized HSA.

Three ways to avoid this headache

The first and most important step is to track your HDHP eligibility month by month. Use a simple spreadsheet or a calendar app to mark which months you are covered by an HDHP. If you change jobs, get written confirmation from your old and new HR departments about the exact dates of coverage. Don't rely on memory — I thought I was covered for 11 months, but my old plan ended on November 30, making me ineligible for December under the proration method.

Second, use HSA calculators from reputable sources like Fidelity or HealthEquity. These tools ask about your coverage months and spit out the maximum you can contribute. They are free and take five minutes. I didn't use one because I thought I knew the rules. A calculator would have flagged the potential issue when I entered “11 months of coverage” and “no HDHP in 2024.”

Third, set calendar reminders for the corrective deadline. The IRS allows you to withdraw excess contributions plus earnings before the tax-filing deadline, including extensions, without penalty. That's typically April 15. If you realize you overcontributed in March, you have a month to fix it. But if you realize in December, you're too late. I set a reminder now for March 1 each year to review my HSA contributions and confirm eligibility.

Additionally, consult IRS Publication 969 annually. It's about 20 pages and covers HSA rules in plain language. The last-month rule is on page 7. I now read it every January, before making any contributions. It takes an hour but could save thousands. Finally, consider automating contributions only after you've confirmed eligibility for the entire year. If you change jobs, pause contributions until you know your new plan qualifies.

What I would do differently next time

If I could go back to November 2023, I would immediately pause all HSA contributions upon leaving my job. Instead, I kept the automatic payroll deductions running through November, which added to the excess. A simple rule: when you leave a job, stop HSA contributions until you verify your new coverage. That alone would have limited my overcontribution to a smaller amount.

I would also keep a spreadsheet of HDHP months, not just for myself but for any spouse or dependents. The IRS counts months of eligibility for each person separately, and if you have family coverage, the proration applies to the family limit. My mistake was only tracking my own months; I didn't consider that my spouse's coverage changed too.

Another change: I would never assume prior months' coverage is sufficient. The last-month rule is an exception, not a default. The default is proration: you can only contribute 1/12 of the annual limit for each month you are eligible. If you rely on the last-month rule, you must be certain you will maintain HDHP coverage for the entire following year. That's a big bet. I now assume proration unless I have a written plan to stay on an HDHP for 12 more months.

Finally, I would ask HR for written confirmation of HDHP coverage dates, not just verbal assurance. My old HR told me my coverage ended on November 30, but I didn't get it in writing. When I later questioned the date, I had no documentation. A simple email with the coverage end date would have clarified my eligibility months and made the proration calculation unambiguous.

The $638 lesson is worth more than the loss

When I first saw the $638 bill, I was angry at the IRS, at my former employer, at myself. But after the anger faded, I realized the lesson was cheap compared to what it could have been. Some people face penalties in the thousands because they overcontribute for multiple years without realizing it. My mistake was caught early, and the total cost, while painful, is less than a typical medical deductible.

That $638, if invested in a broad market index fund for 30 years, could have grown to roughly $2,000 at a 4% real return. So yes, it stings. But the knowledge I gained — about the last-month rule, the testing period, and the importance of tracking eligibility — will prevent future penalties that could be much larger. I now check HSA rules before any life change: job switch, marriage, childbirth, or even a move to a different state with different insurance options.

I share this story so others can skip the same mistake. One form, one deadline, one rule — that's all it takes to turn a tax-advantaged account into a tax headache. The HSA is still a powerful savings tool, but it demands respect for its rules. If you treat it casually, it will cost you. If you treat it carefully, it can save you thousands in taxes over a lifetime. My $638 is a small price for that reminder.

This article is for informational purposes only and does not constitute tax or legal advice. Consult a qualified professional regarding your specific situation.