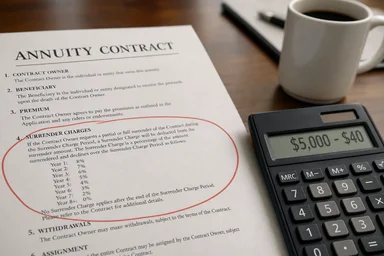

My Annuity Contract Charged a $5,000 Surrender Fee for a $40 Monthly Withdrawal

When Susan Chen, a 68-year-old retired teacher in Ohio, wanted to take $40 a month from her fixed annuity to cover a small recurring expense, she didn't expect a fight. She had owned the policy for six years, had never withdrawn more than the allowed free amount, and assumed the modest sum would slide under the radar. Instead, her insurance company deducted a $5,000 surrender fee from the withdrawal—125 times the amount she requested. The insurer cited a clause buried on page 27 of the contract: any withdrawal exceeding the annual free allowance triggers a full surrender charge on the entire payment. Chen's story, shared with state regulators, is not an isolated case. As of early 2024, the Ohio Department of Insurance had logged over 200 similar complaints since 2020. This article explores how such outsized fees happen, what protections exist, and how to steer clear of them.

Understanding Surrender Charges

A surrender charge is a fee imposed by an insurance company when you withdraw money from an annuity beyond the allowed free amount. These fees are designed to discourage early withdrawals and to compensate the insurer for the costs of issuing the policy, including commissions paid to agents and administrative expenses. Surrender charges are typically a percentage of the withdrawal amount, but as Susan Chen discovered, they can also be calculated on the entire account value or the entire withdrawal, depending on the contract language. The percentage usually declines over time, often starting at 7-10% in the first year and decreasing by one percentage point each year until it reaches zero after seven to ten years. However, some contracts have more complex rules, such as a "market value adjustment" that can increase the fee when interest rates are rising. For example, if interest rates have risen sharply since the annuity was purchased, the market value of the underlying bonds may have dropped, and the insurer may impose an additional adjustment on top of the surrender charge. This can result in a total penalty of 15% or more of the withdrawal amount. Understanding the specific terms of your contract is crucial, as variations can significantly impact the cost of accessing your money.

Why Insurers Impose Surrender Fees

Insurance companies rely on the long-term nature of annuity contracts to manage their investment portfolios. When you purchase an annuity, the insurer invests your premium in bonds, mortgages, and other long-term assets that generate predictable returns. If you withdraw money early, the insurer may have to sell those investments at a loss, especially if interest rates have risen. The surrender charge helps offset that potential loss and also recoups the upfront costs the insurer incurred to sell and service the policy. For example, the agent who sold the policy may have received a commission of 5-7% of the premium, which the insurer expects to recover over time through fees and investment spreads. If you leave early, the surrender charge ensures the insurer isn't left holding the bag. Additionally, insurers use a concept called "matching" to align the duration of assets and liabilities. An annuity contract is a long-term liability, and the insurer invests in long-term assets to match it. Early withdrawals disrupt this matching, forcing the insurer to liquidate assets prematurely, which can lock in losses. The surrender fee compensates for this disruption. From the insurer's perspective, these fees are not punitive but rather a mechanism to maintain fairness among policyholders. Without them, those who stay in the contract would subsidize those who leave early through lower returns or higher fees.

Free Withdrawal Provisions: What You Need to Know

Most annuity contracts include a free withdrawal provision, also known as a "penalty-free withdrawal" or "free corridor," that allows you to take out a certain amount each year without incurring a surrender charge. Typically, this is 10% of the account value, but it can vary. For example, some contracts allow 10% of the initial premium, while others allow 10% of the current account value. However, as Susan Chen's case shows, the free withdrawal provision may not apply to systematic withdrawals or may be calculated on an annual basis, meaning that if you take out $40 each month, the total annual withdrawal of $480 may exceed the free allowance if the account value is low. In Chen's case, her annuity had a cash value of $50,000, so the 10% free allowance was $5,000 per year. She withdrew $480 in total, well under the allowance. So why did she get charged? Because the contract's fine print stated that any withdrawal that is part of a systematic withdrawal program—even if under the free allowance—triggers a full surrender charge on the entire payment. This is a common but often overlooked clause. Another nuance is that some contracts require you to take free withdrawals as a lump sum rather than in installments. For instance, if you want to take $5,000 once per year, it might be allowed without penalty, but taking $416.67 per month would trigger charges. Always check whether your contract distinguishes between systematic and non-systematic withdrawals. Some insurers also limit the free withdrawal to the first withdrawal of the year, meaning subsequent withdrawals in the same year are subject to surrender charges even if the total is under the limit.

Real-World Examples of Surprise Surrender Fees

Susan Chen's experience is far from unique. In 2022, a retiree in Florida named Robert Martinez tried to withdraw $200 from a variable annuity to pay a utility bill. His contract had a free withdrawal provision of 10% of account value, but the insurer charged a $3,200 surrender fee because the withdrawal was processed as a partial surrender rather than a free withdrawal. The contract required that free withdrawals be requested in writing at least 30 days in advance, and Martinez had used an online portal that didn't qualify. Another case involved a California woman, Linda Park, who had a fixed-indexed annuity with a "lifetime income rider." She wanted to take her required minimum distribution (RMD) from the annuity, but the insurer applied a surrender charge because the RMD was not considered a free withdrawal under the contract. She had to pay a $2,500 fee on a $1,800 RMD. These examples highlight the importance of reading the contract carefully and understanding the specific rules for free withdrawals. A third example comes from Texas, where a retiree named James Thompson had a fixed annuity with a 7-year surrender schedule. In year 5, he needed $10,000 for a medical emergency. He assumed the surrender charge would be 3% (the schedule showed 3% in year 5), but the contract also included a market value adjustment that added another 4% because interest rates had risen. His total fee was $700, which he had not anticipated. While not as dramatic as Chen's case, it still caused financial strain. These stories underscore the need to ask about all potential fees, not just the base surrender charge.

The Trade-Off: Higher Returns vs. Liquidity

Annuities offer benefits like tax-deferred growth, guaranteed income, and protection from market downturns. However, these benefits come at the cost of liquidity. Surrender charges are the price you pay for the insurer's long-term commitment. For investors who are confident they won't need access to their money for seven to ten years, the higher returns offered by some annuities (compared to CDs or bonds) may be worth the surrender charge risk. For example, a fixed annuity might offer a 3% interest rate, while a five-year CD offers 2.5%. Over ten years, the annuity's higher rate could offset the surrender charge if you don't need to withdraw early. But if you have any uncertainty about your cash needs, a more liquid investment like a CD or a bond ladder might be a better choice. Financial planners often recommend keeping an emergency fund of six to twelve months of expenses in liquid assets before investing in annuities. Additionally, consider the concept of "opportunity cost." If you invest in an annuity and later need to withdraw money early, the surrender fee may wipe out years of interest gains. For instance, if you invest $100,000 in an annuity earning 3% and need to withdraw $20,000 in year 3, a 7% surrender charge would cost $1,400, which is more than the interest earned on that $20,000 over three years (about $1,855 in total interest on the full $100,000, but only a portion of that is attributable to the $20,000). So, while the annuity may have a higher headline rate, the net return after fees can be lower than a more liquid alternative. On the other hand, for those who hold the annuity to term, the higher rate can be beneficial. The key is to align the investment with your expected liquidity needs.

How to Avoid Surrender Fee Surprises

To avoid a situation like Susan Chen's, take these steps before purchasing an annuity or making a withdrawal. First, read the contract thoroughly, especially the sections on surrender charges, free withdrawals, and systematic withdrawal programs. Look for language like "any withdrawal under this program is subject to surrender charges" or "free withdrawals are not available for systematic payments." Second, ask the insurance company or your agent for a written explanation of how free withdrawals work. Get it in writing. Third, consider using a financial planner who is a fiduciary, meaning they are legally required to act in your best interest. A fee-only planner can help you evaluate whether an annuity is suitable for your situation. Fourth, if you already own an annuity and need to make a withdrawal, contact the insurer directly and ask about surrender charges before initiating the transaction. Request a surrender charge schedule in writing. Fifth, if you are considering a systematic withdrawal, ask whether each withdrawal is treated separately or aggregated for the free allowance. Some contracts allow you to take a lump-sum free withdrawal once per year, but systematic withdrawals may be subject to charges. Sixth, consider setting up a free withdrawal for the maximum allowed amount once per year, rather than taking smaller monthly amounts. For example, if your free allowance is 10% of $50,000 ($5,000), take the full $5,000 in January and then budget that money to last the year. This avoids any confusion about systematic withdrawals. Seventh, keep a copy of your contract in an easily accessible place, and review it annually. Insurance companies sometimes change their policies or interpretations, so staying informed is important.

What to Do If You've Been Charged an Unexpected Surrender Fee

If you believe you were charged a surrender fee in error or that the contract language was misleading, you have options. First, contact the insurance company's customer service department and ask for a detailed explanation of the fee. Request a copy of the contract provision that authorizes the charge. If you are not satisfied, escalate to a supervisor. Second, file a complaint with your state's insurance department. State regulators have the authority to investigate unfair or deceptive practices. In Susan Chen's case, she filed a complaint with the Ohio Department of Insurance, which mediated a settlement for a partial refund. Third, consider consulting an attorney who specializes in insurance law. Some attorneys offer free consultations. Fourth, if the annuity was sold by a broker or agent, you may be able to file a complaint with the Financial Industry Regulatory Authority (FINRA) or the Securities and Exchange Commission (SEC) if the annuity is a registered security. Fifth, you can also contact the Better Business Bureau or leave a review on consumer websites to warn others. Additionally, check if your state has a "free look" period that might apply. While the free look period is typically for new purchases, some states allow a grace period for certain changes. If you were charged a fee within the first few days of a new contract, you might be able to cancel without penalty. Also, consider reaching out to a consumer advocacy group like the National Association of Insurance Commissioners (NAIC) for guidance. They have resources on how to file complaints and what information to include.

Counter-Arguments: The Insurer's Perspective

It's easy to see surrender fees as punitive, but insurers argue they are necessary to keep premiums affordable for all policyholders. Without surrender charges, insurers would have to charge higher fees or offer lower returns to compensate for the risk of early withdrawals. For example, if every policyholder could withdraw money at any time without penalty, the insurer would have to hold more cash reserves, reducing investment returns. Surrender charges also allow insurers to offer guaranteed income options, such as lifetime withdrawal benefits, which require a long-term pool of assets. In addition, surrender charges are disclosed in the contract, and most states require insurers to provide a free-look period (typically 10 to 30 days) during which you can cancel the policy without penalty. So, while the fees can be surprising, they are not hidden. The challenge is that many consumers don't read the fine print or don't understand the implications of complex contract language. Insurers also point out that surrender charges are a standard feature of many financial products, not just annuities. For instance, some mutual funds have back-end loads that decrease over time, similar to annuity surrender schedules. The difference is that annuity contracts often have longer durations and more complex rules. Moreover, insurers argue that they are heavily regulated and must file their contract forms with state insurance departments, which review them for compliance. If a fee is deemed unfair, regulators can reject the form. So, from a legal standpoint, the fees are legitimate. However, critics counter that the complexity of the language can be a form of obfuscation, and that regulators may not catch every problematic clause. The debate highlights the need for clearer disclosure standards.

Alternatives to Annuities for Retirement Income

If the surrender charge issue makes you wary of annuities, consider other retirement income strategies. A bond ladder, for example, involves buying bonds with staggered maturities so that a portion matures each year, providing cash flow without penalties. A dividend-paying stock portfolio can provide income, though it carries market risk. A systematic withdrawal from a 401(k) or IRA can be set up without surrender charges, though you'll pay income tax on withdrawals. Another option is a CD ladder, where you buy CDs with different maturity dates; early withdrawal penalties are typically limited to a few months of interest, far less than annuity surrender charges. For those who want guaranteed income, a single-premium immediate annuity (SPIA) can provide lifetime payments without ongoing surrender charges, but you give up access to the principal. Each option has trade-offs, and the best choice depends on your individual needs and risk tolerance. For example, a bond ladder offers more flexibility but may provide lower yields than an annuity. A dividend portfolio can grow over time but is subject to market volatility. A CD ladder is safe but offers low returns in a low-interest-rate environment. A SPIA provides guaranteed income but no liquidity. Some investors combine strategies, such as using a CD ladder for near-term expenses and an annuity for long-term income. The key is to match the investment's liquidity profile with your expected cash needs. For instance, if you have a large one-time expense coming up in five years, a five-year CD might be better than an annuity with a seven-year surrender period. Alternatively, if you are healthy and expect to live a long time, an annuity's lifetime income might outweigh the surrender risk.

Conclusion

Susan Chen's $5,000 surrender fee on a $40 withdrawal is a cautionary tale about the importance of understanding annuity contract terms. Surrender charges are a common feature of deferred annuities, but they can be triggered in unexpected ways, especially when systematic withdrawals are involved. By reading the fine print, asking questions, and working with a fiduciary financial planner, you can avoid similar surprises. If you do face an unexpected fee, don't hesitate to contact the insurer and state regulators. While annuities can be a valuable part of a retirement plan, they are not one-size-fits-all products. Always weigh the benefits of tax deferral and guaranteed income against the costs of reduced liquidity. With careful planning, you can make informed decisions that protect your retirement savings from unnecessary fees. Remember that knowledge is your best defense: the more you understand about your contract, the less likely you are to be caught off guard. Whether you choose an annuity or an alternative, the goal is to create a retirement income strategy that meets your needs without unexpected penalties.